Is Your Dinner Deciding When You Can Retire? How Cooking at Home Could Add $200k to Your Retirement Fund.

Key Takeaways

CNET estimates that Millennials spend $86.55 per week on takeout—$4,500 per year.

Third-party delivery apps carry a markup of nearly 70%—for every $100 spent, $41 is going toward platform fees.

We throw away ~30% of our food—food that requires 4.2 trillion gallons of irrigation water to produce, amounts to more than 1,250 calories, and costs ~$728 per person annually.

Reducing takeout isn't just about saving money; it means reclaiming a nutrient-dense diet and potentially adding $200k+ to your retirement through compound interest.

Disclaimer: I am not a financial advisor. The information in this post is for educational and entertainment purposes only and should not be construed as professional financial, investment, or tax advice. Investing involves risk, including the possible loss of principal. Historical returns are not a guarantee of future results. Please consult with a licensed professional before making any significant financial decisions.

Is Your Dinner Deciding When You Can Retire?

It’s 6:00 PM, your brain is "fried," and you have nothing in the fridge for dinner. Either that or your leftovers just aren't calling your name. Your brain has been running tabs all day—emails, Slack notifications, that weirdly passive-aggressive comment from your boss—and just the thought of chopping an onion makes your eyes burn.

So, you do what any sensible human in 2026 does: you pull out your phone. You scroll. You see a picture of a steaming bowl of ramen or tacos al pastor. You tap "order," pay the $12 in fees without looking too closely at the total, and feel that tiny hit of dopamine when the app tells you your food is 22 minutes away.

We’ve all been there. I’ve been there. In fact, most of us live there. But while we’re busy "saving time" by outsourcing our dinner, we’re accidentally cutting into our retirement fund. It’s an easy trade to make in the moment. We tell ourselves we're just avoiding the late night run to the grocery store and the sink full of dishes. And let's be honest, we could all use the mental break once in a while—it would just be great to avoid the bank statement littered with takeout charges.

How much does my takeout actually cost?

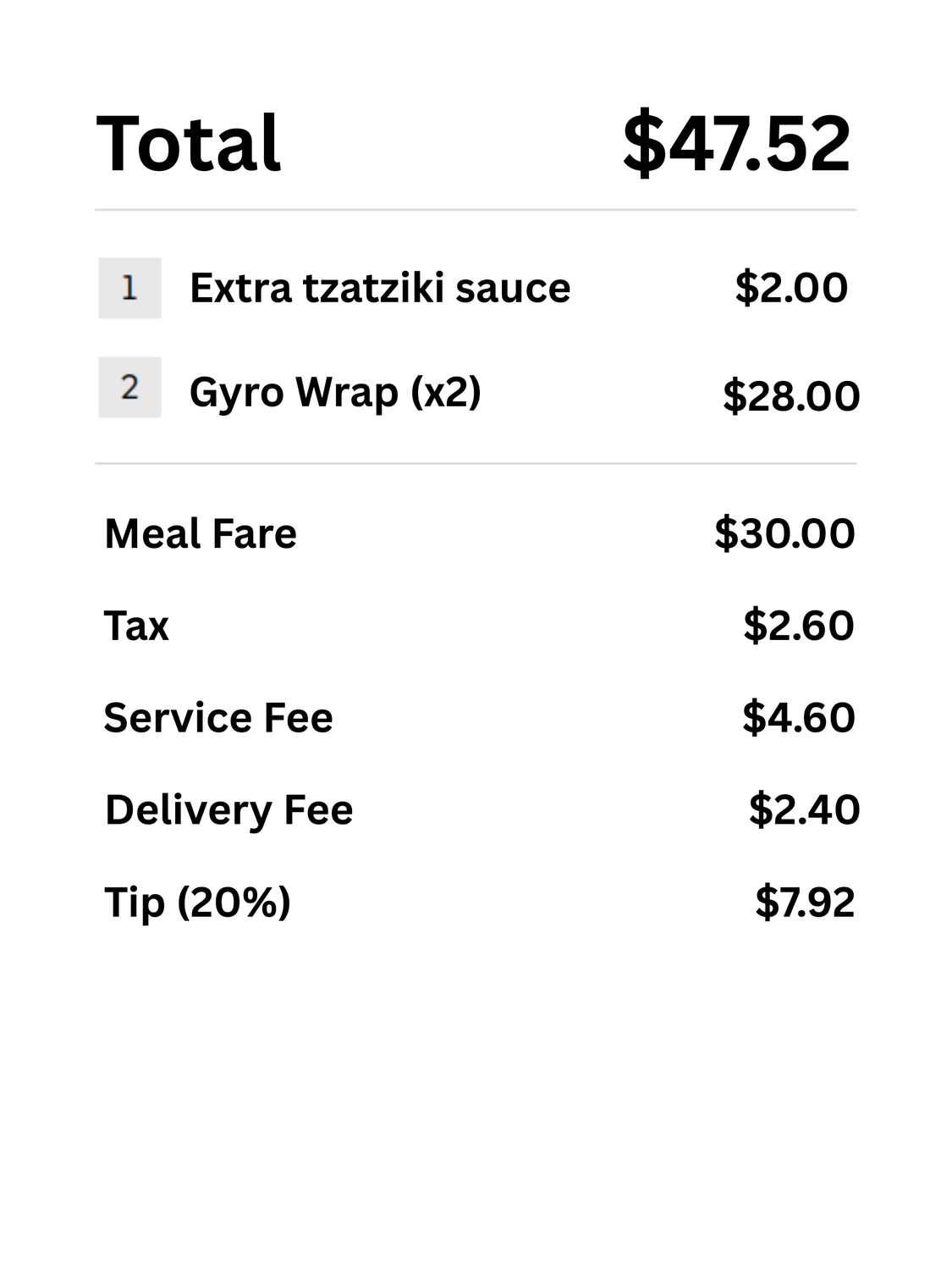

When you order delivery, you aren't just paying for food. You’re paying for the sales tax, service fee, delivery fee (if applicable) and, oh yeah, let's not forget the 20% tip. Recent industry data from Self found that the average markup on third-party delivery apps like DoorDash and UberEats is now ~70%. So, by the time you're done, that $30 meal is nearing $50 and you're wishing it were a little LESS convenient to order out.

The average markup on third-party delivery apps like DoorDash is ~70%—turning a $30 dinner into a ~$50 regret.

According to a Consumer Dining Survey by CNET, Millennials spend $86.55 per week on takeout. That's roughly $4,500 a year. Wait, did I just book a trip to the Maldives...?

The sting isn't just in the total; it’s in the breakdown. Because of that 70% markup, roughly $1,800 of your yearly spend isn't going toward high-quality ingredients or supporting your favorite local chef—it’s disappearing into the 'digital infrastructure.'

By defaulting to takeout, the cost is two-fold. Not only are you forfeiting a higher-protein, more nutrient-dense diet in exchange for sluggishness and increased future medical costs; you're also missing out on loads of compound interest that will make for a more "comfy" retirement.

How much food am I wasting?

Money spent on takeout isn't the full picture—it's also the $15 we spent on organic Kale that we slowly watch wilt in the back of the fridge because we didn't have a plan for it. Or the basil, fish sauce, and container of curry paste that we desperately needed for our "Authentic Thai Basil Chicken"—sounds great on Sunday, but because we bought 'by the recipe,' we're now staring down five days of Thai curry for lunch just to use up the paste. No wonder the delivery app looks so tempting by Thursday.

Americans waste 30% of their food—worth more than 1,250 calories per day, 4.2 trillion gallons of irrigation water, and $728 in annual costs

According to research from Wiley Online and the EPA, the average American tosses 30% of their food—a habit that wastes 4.2 trillion gallons of irrigation water annually. On a personal level, that’s over 1,250 calories per day thrown in the bin and a $728 hit to your bank account every year.

Why does this happen? Because traditional meal planning is broken. It asks us to shop for recipes instead of ingredients. When you shop for recipes, you end up with a fridge full of "single-use assets" that don't play well together. You have 3/4 container of curry paste, pine nuts, and a lone zucchini. None of those make a meal, so you get frustrated, give up, and—you guessed it—order takeout.

The alternative is using a better system to plan your weekly meals. Imagine opening your fridge and seeing organized proteins, vegetables, your favorite sauce, and a few pantry staples that you can easily turn into a 15-minute meal. It's the difference between staring at a puzzle you can't solve and having peace of mind that you don't need to spend the next hour and a half figuring out what to eat.

Can Your Takeout Habit Fund Your Retirement?

Say you've cut back on takeout and have a new system in place, but you're stuck wondering what to do with the excess money you're saving from cooking all of those delicious meals at home. This is where things get exciting—rather than letting that extra money sit in your bank account earning 0.1% interest, transfer it into a standard index fund averaging 7% (inflation-adjusted) annual returns.

If you're asking, "Where can I look for 7% returns?", a common starting point is a total market or S&P 500 index fund that has a low expense ratio (e.g. 0.02% to 0.04%). You'll want to stick with ETFs vs. mutual funds (to start) since ETFs are usually free to trade across platforms. Buy VTI (ETF), for example, instead of VTSAX (mutual fund) on platforms other than Vanguard to avoid paying a $49.95 - $74.95 fee every time you add to the fund. I've added some standard index funds below as a starting point.

Quick Reference: Finding the Right Fund for Your Platform

If you use...

Vanguard

S&P 500 Index Fund: VOO (or VTSAX)

Total Market Index Fund: VTI (or VTSAX)

Schwab

S&P 500 Index Fund: SWPPX

Total Market Index Fund: SWTSX

Fidelity

S&P 500 Index Fund: FXAIX

Total Market Index Fund: FSKAX

If you use...

Vanguard

Schwab

Fidelity

S&P 500 Index Fund

VOO (or VTSAX)

SWPPX (or VOO)

FXAIX

Total Market Index Fund

VTI (or VTSAX)

SWTSX (or VTI)

FSKAX

While the market has daily ups and downs, these funds help you effortlessly manage risk by spreading your investment across hundreds of industry-leading companies—from tech giants to healthcare staples—leveraging a strategic approach to investing that has supported historical average 7% annual returns since 1957. When investing in an S&P 500 index fund, you're purchasing a small portion of 500 different stocks; or anywhere from 3,000 to 4,000 stocks when placing your money in a total market index fund.

Once you’ve found a home for that $100 a week you used to spend on delivery fees and wilted groceries—roughly $430 a month—you can start to build up your 401(k), Roth IRA, or personal brokerage account. Whether you’re padding your retirement or planning on quitting your 9-to-5 before the age of 50, here is how that consistency compounds when starting from zero:

In 10 years, you could have $74,000.

In 20 years, you could have $224,000.

And that's the $200k Retirement Gap! As I'm sure you've heard in the past, time is everything when it comes to investing. It's not a get rich quick scheme that is going to take your account balance from $0 to $1M overnight. You CAN, however, see exponential growth once you hit the $100k mark—If you take that same $430/month and add it to your $100k brokerage account, that same $430 monthly investment turns into $627,000 over 20 years. That's a $400k difference.

In Conclusion.

Adding $200k to your retirement doesn’t require you to become a Michelin-star chef or spend your entire Sunday meal prepping like a fitness influencer with 40 identical plastic containers. In fact, that kind of rigidity is exactly why most people fail.

By shifting from "scrolling for recipes" to prepping ingredients—3 veggies, 2 proteins, and a couple of sauces—you reclaim 90 minutes of your night and $100 of your weekly budget.

When you’re ready to start, keep it simple:

Pick 3-4 veggies that you actually enjoy

Pick 2-3 proteins

Master 1-2 flavor profiles (like a killer lemon-herb or a spicy soy ginger) that can tie any combination together.

If you want a system that does the heavy lifting for you—from ingredient-based planning to automated grocery lists—get the Flavor and Thyme app. Stop over-complicating dinner and let's start building that $200,000 bridge together.

You deserve a future where you aren't stressed about money. And it turns out, that future might just be sitting in your grocery bag.

Disclaimer: I am not a financial advisor. The information in this post is for educational and entertainment purposes only and should not be construed as professional financial, investment, or tax advice. Investing involves risk, including the possible loss of principal. Historical returns are not a guarantee of future results. Please consult with a licensed professional before making any significant financial decisions.

Resources & Deep Dives

2024 Diner Dispatch Survey (US Foods): Average person dines out 4.6x per month; takeout 3x per month in 2024

2025 Off-Premises Restaurant Trends (National Restaurant Association): Highlights that 67% of Millennials now view takeout as "essential" to their lifestyle, with nearly 75% of all restaurant traffic now happening off-premises.

2025 Consumer Dining Survey (CNET): Millennials spend $86.55 per week on takeout—$4,500 per year.

Taste Test: Where Consumers Are Dining Out (Bank of America Institute, Feb 2026): Real-time internal card data showing that high-income Millennials and Gen Z are the primary drivers of restaurant and delivery growth, despite rising menu prices.

Food Delivery Statistics (Toast POS): An industry report revealing that 20% of professionals aged 25–34 are "power users," ordering delivery 6–10 times per month.

"Estimating the Cost of Food Waste to American Consumers" (2025 EPA report) (Full Report): A typical family of four now spends roughly $2,913 annually on food they never eat—$728 per person.

Household food waste trending upwards in the United States: Insights from a National Tracking Survey: After food leaves the farm in the United States, approximately 30% (66.5 million tons) is wasted. Producing this lost and wasted food requires... 4.2 trillion gallons of irrigation water... with the uneaten food representing greater than 1250 calories and about one pound of food per capita per day

The Most Expensive Cities for Food Delivery in the U.S.: In 2025, the average order cost $36.95 directly from McDonald's, or an average of $57.87 when delivered via third-party apps. DoorDash is the most expensive food delivery app - costing $63.21 (71.1% higher than buying directly from McDonald’s).

Compound Interest Calculator: Investor.gov Determine how much your money can grow using the power of compound interest.

What Is the S&P 500 Average Annual Return?: This confirms the ~10% nominal / ~7% real return baseline used by almost every financial planner.

POST CATEGORY

EAT WELL

SAVE MONEY

PLAY THE LONG GAME.

Created with systeme.io